I remember the first time I sat across the desk from a loan officer. I was 24, my car had just blown a transmission, and I needed $3,000 yesterday.

The guy in the cheap suit slid a piece of paper across the desk. I looked at the number. 18%.

I felt sick. I felt cornered. But mostly, I felt stupid because I didn’t know if that number was normal or if I was being taken for a ride. I signed it because I was desperate. I spent the next three years paying for that transmission twice over.

Ten years and thousands of client consultations later, I’m the guy on the other side of the desk. And I promise you this: You do not have to feel that way.

If you are staring at a loan offer right now, sweating over the fine print, asking yourself, “What is a reasonable interest rate for a personal loan?”—take a breath.

We are going to decode this together. No banking jargon. No judgment. Just the raw numbers and the strategy you need to keep your money in your pocket, not the bank’s vault.

The Short Answer (What You Came For)

Let’s rip the band-aid off. You want a number? Here is the reality of the market right now.

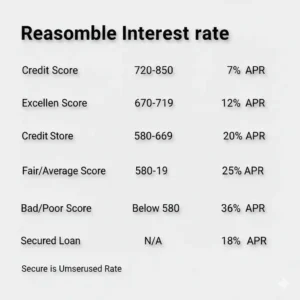

A “reasonable” rate isn’t a single number; it’s a range based on how much the bank trusts you.

As of right now, the national average for a personal loan hovers around 12% to 15%. But averages are misleading. If you have excellent credit, 12% is an insult. If you have bad credit, 12% is a miracle.

Here is my “Reasonable Rate” Cheat Sheet based on your credit tier:

- Excellent Credit (760 – 850):

- Target: 6% to 9%

- Verdict: This is the VIP section. Lenders will fight for you.

- Good Credit (700 – 759):

- Target: 10% to 14%

- Verdict: This is standard. You represent a low risk, but you aren’t getting the “doorbuster” specials.

- Fair Credit (640 – 699):

- Target: 15% to 22%

- Verdict: We are entering the danger zone. The loan is expensive, but it might still beat a credit card.

- Bad Credit (Below 640):

- Target: 23% to 35%

- Verdict: Stop. Proceed with extreme caution. At this level, the interest is predatory.

The Golden Rule: If your personal loan rate is higher than your credit card interest rate (usually 20-25%), walk away. The whole point of a personal loan is to save money on interest, not pay more.

The “Black Box”: Why Did They Give Me That Rate?

Most people think their credit score is the only thing that matters. That’s false.

I’ve seen clients with a 750 score get denied or slapped with high rates, while a guy with a 680 gets a decent deal. Why? Because banks are essentially casinos. They are calculating the odds of you folding your hand (defaulting).

Here are the three invisible levers that change your rate:

1. The Debt-to-Income Ratio (DTI)

This is the number one deal-breaker I see.

The bank looks at how much money you make versus how much you already owe.

- Scenario: You make $100k a year (great!). But you spend $6k a month on mortgage, car notes, and student loans.

- Bank’s View: You are “house poor.” You have no wiggle room. They will hike your rate to cover the risk.

2. The Loan Term (Length)

This is simple physics. The longer you hold the money, the more it costs.

- 3-Year Loan: Lower interest rate. Higher monthly payment.

- 5-Year Loan: Higher interest rate. Lower monthly payment.

Pro Tip: Always pick the shortest term you can comfortably afford. A 5-year loan might look cheaper monthly, but you could end up paying thousands more in interest.

3. Secured vs. Unsecured

Most personal loans are unsecured. This means you promise to pay it back, but you aren’t putting up your house or car as collateral. Because the bank has nothing to grab if you run away, they charge you more.

If you have a savings account or a vehicle, asking for a secured loan can drop your rate by 3-4% instantly.

The Trap: Interest Rate vs. APR

This is where they get you. This is where 90% of my clients get confused.

You see a big bold number: 9% Interest!

But in the fine print, you see: 12% APR.

What is happening?

- Interest Rate: The cost of borrowing money.

- APR (Annual Percentage Rate): The cost of borrowing the money, PLUS the fees they charge to set it up.

The biggest culprit is the Origination Fee.

Many online lenders charge a fee just to process the paperwork. It usually ranges from 1% to 8% of the loan amount. They deduct this from the cash they send you.

Example:

You borrow $10,000.

The lender charges a 5% origination fee ($500).

You only receive $9,500 in your bank account, but you still owe interest on the full $10,000.

My Advice: When comparing loans, ignore the interest rate. Only look at the APR. The APR is the only number that tells the truth about the total cost.

4 Red Flags That Scream “Rip-Off”

In my years of helping people dig out of debt, I’ve seen some nasty contracts. If you see these signs, run.

1. Prepayment Penalties

This makes my blood boil. Some lenders will fine you for paying off the loan early. They do this because they want to milk you for every cent of interest.

Action: Never sign a loan with a prepayment penalty. You want the freedom to crush that debt if you get a bonus or tax refund.

2. “Guaranteed Approval”

If an ad says “No Credit Check” or “Guaranteed Approval,” it is not a loan. It is a trap. These are often payday loans in disguise with APRs hitting 400%.

3. Upfront Insurance

If they ask you to buy “credit insurance” to protect the loan in case you die or lose your job, say no. It’s an expensive upsell that rarely pays out.

4. Variable Rates

Personal loans usually have fixed rates (the payment never changes). Some lenders offer “variable” rates that start low but can skyrocket if the Federal Reserve raises rates. In this economy? Stick to fixed.

The “Secret Sauce”: The 48-Hour Rate Match

Okay, here is the trick that you won’t find on the front page of Google. Most people treat loan rates like price tags at a grocery store—fixed and non-negotiable.

They are wrong.

Loan officers, especially at local Credit Unions and smaller banks, have discretion. They have quotas to hit.

Here is the “Rate Match” strategy I teach my clients:

- Get a Baseline: Go to an online marketplace (like SoFi, LendingClub, or Upstart) and do a “Soft Pull” to see your rate. Let’s say they offer you 11%.

- The Screenshot: Take a screenshot of that offer.

- The Walk-In: Walk into a local Credit Union. (If you aren’t a member, join. It’s usually $).

- The Script: Sit down and say, “I have an offer for 11% online. I’d much rather keep my business local with you guys. Can you beat this rate, or at least match it with lower fees?”

Why this works:

Credit Unions are non-profits. They aren’t trying to squeeze you for shareholder dividends. I have seen Credit Unions undercut online lenders by 2% just to get a reliable borrower on their books.

Bonus Move: If you have decent assets but cash flow issues, ask for a “Share Secured Loan.” You lock up money in a savings account as collateral, and they loan it back to you at a tiny interest rate (often 2-3% above the savings rate). It builds credit incredibly fast and costs very little.

Your Action Plan: How to Get the Best Rate Today

Reading about it is nice. Doing it is better. If you need a loan, follow this exact sequence to ensure you get a reasonable rate.

Step 1: Clean Up Your “Utilisation”

Before you apply, look at your credit cards. Are they maxed out?

Your Credit Utilisation (how much of your limit you are using) makes up 30% of your score.

- The Hack: If you can, pay down your balances a few weeks before applying. Even dropping your utilisation from 80% to 50% can bump your score by 20 points. That 20-point bump could move you from “Fair” to “Good” and save you 4% in interest.

Step 2: The Soft Pull Shopping Spree

Go to 3 different online lenders. Fill out their pre-qualification forms.

Crucial: Make sure they state it is a “Soft Credit Check.”

This lets you see real rates without hurting your score.

- Lender A: 12%

- Lender B: 14%

- Lender C: 11.5%

Step 3: Check the “Fine Print” Fees

Take your top two offers and hunt for the Origination Fee.

- Lender A (12%) has $0 fees.

- Lender C (11.5%) has a $400 fee.

- Winner: Lender A is likely cheaper in the long run, even with the higher rate.

Step 4: The Credit Union Check

Take the winner from Step 3 and try the “Secret Sauce” tactic at a local branch.

Step 5: The 24-Hour Cool Down

Once you are approved, wait 24 hours.

Emotions lead to bad financial decisions. Sleep on it. Read the contract with fresh eyes in the morning. Check specifically for the prepayment penalty clause.

If it looks good, sign.

When a Personal Loan is a Bad Idea (Even with a Good Rate)

I want to be your friend here, not a salesman. Sometimes, the most reasonable interest rate is 0%—because you shouldn’t take the loan at all.

Do not take a personal loan for:

- Vacations: If you have to borrow money to relax, you won’t relax. You’ll just be stressed on a beach.

- Weddings: Start your marriage with love, not debt.

- Speculative Investments: Never borrow money to buy crypto or stocks. That is gambling, not investing.

Personal loans are tools. They are best used for Debt Consolidation (killing high-interest credit cards) or Home Improvement (adding value to an asset).

Conclusion: You Are in the Driver’s Seat

So, what is a reasonable interest rate for a personal loan?

It’s the rate that allows you to solve your problem without creating a bigger one down the road.

If you have good credit, fight for that 10-12% range.

If you have excellent credit, demand single digits.

If you are being offered 25%+, pause. Take a step back. Look at other options like 0% balance transfer cards or a side hustle to generate cash.

The banks want you to feel small. They want you to feel like they are doing you a favour by lending you money.

Flip the script.

You are the customer. You are the revenue source. Shop around, ask tough questions, and don’t sign anything until the math makes sense to you.

You’ve got this. Now go check your rates, but keep your wallet closed until you see the right number.

Frequently Asked Questions

1. Does checking my rate hurt my credit score?

Not if you do it right. Most lenders now offer a “pre-qualification” tool that uses a soft inquiry. This does not touch your score. Your score is only impacted (a hard inquiry) when you actually submit the final application to accept the loan.

2. Can I get a personal loan with a 500 credit score?

Technically, yes. But it will be ugly. You are looking at rates of 30% to 35%, which is borderline predatory. At that level, you are better off looking into credit counselling or secured credit cards to build your score up first.

3. Why is my personal loan rate higher than my car loan rate?

Because a car loan is secured. If you stop paying, the bank comes with a tow truck and takes the car. With a personal loan, they have no physical asset to take, so they charge you more to cover that risk.

4. How long does it take to get the money?

It’s fast. Online lenders can often deposit money into your account within 24 to 48 hours. Traditional banks and credit unions might take 3 to 7 days.

5. Is a fixed rate or a variable rate better?

For personal loans, Fixed is King. A fixed rate guarantees your monthly payment never changes, no matter what the economy does. It gives you stability and peace of mind