Let me take you back to 2011.

I was sitting in a bank office that smelled like stale coffee and floor wax. I was wearing my only suit, sweating through my shirt, trying to convince a guy named “Bob” that I was responsible enough to borrow $150,000.

I had spent years eating ramen, saving every penny, terrified that if I didn’t have a massive 20% down payment, I’d be laughed out of the building. I was nervous, confused, and honestly, I felt like a fraud.

Bob looked at my paperwork, sighed, and said, “You know you didn’t need to wait this long, right? You could have bought this house three years ago.”

I almost flipped the desk.

I had wasted three years paying rent because I didn’t understand the rules of the game. I thought there was only one way to buy a house: Perfect credit and a mountain of cash.

I was wrong. And if you are reading this, chances are you are feeling that same anxiety I felt. You are drowning in acronyms—FHA, USDA, VA, ARM—and wondering if you’ll ever get the keys.

Here is the truth: You don’t need 20% down. You don’t need a perfect 800 credit score. You just need the right product.

Today, we are going to cut through the banking noise. I’m going to walk you through the different types of mortgage loans for first-time buyers, not like a banker, but like a friend who wants you to stop throwing money away on rent.

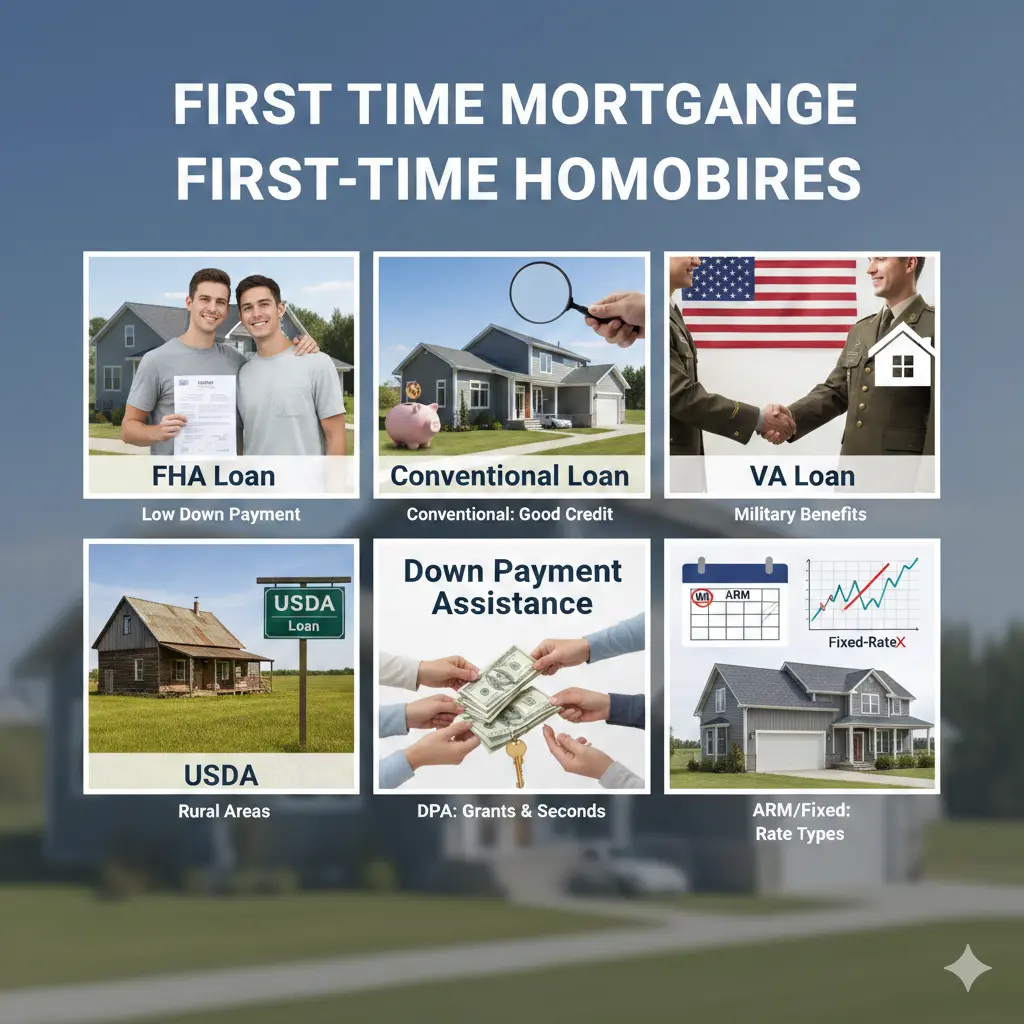

The “Big Three” (Plus the Hidden Gems)

When you start shopping for a mortgage, it feels like walking into a restaurant with a menu in a different language. Let’s translate it.

There are really only three main categories you need to care about right now, plus a few “speciality” flavours if you fit a specific profile.

1. The Conventional Loan (The “Standard” Choice)

This is what most people think of when they hear “mortgage.” It’s a loan that isn’t backed by the government. It’s just between you and the bank (mostly).

The Myth: “You need 20% down for a conventional loan.”

The Truth: First-time buyers can get in for as little as 3% down.

This is called the “Conventional 97” program (offered through Fannie Mae or Freddie Mac).

- Who is this for?

If you have decent credit (usually 620+) and want the cheapest long-term option, start here. - The Pros:

- PMI Removal: This is the biggest win. Private Mortgage Insurance (PMI) is an extra fee you pay when you put less than 20% down. On a conventional loan, once you pay down enough of the house (reach 20% equity), that fee disappears forever.

- Flexibility: Sellers love these loans. In a bidding war, a conventional pre-approval letter looks “stronger” to a seller than a government-backed loan.

- The Cons:

- Stricter Credit: If your score is below 620, getting approved is tough. If it’s below 680, your interest rate might be higher than you’d like.

- Debt-to-Income (DTI): They are strict about how much debt you carry relative to your income.

My Take: If your credit score is solid (680+), fight for this loan. Being able to eventually drop that PMI payment without refinancing is a massive financial win.

2. The FHA Loan (The “Second Chance” Hero)

FHA stands for the Federal Housing Administration. The government doesn’t lend you the money; they just insure the bank against your defaulting. Because Uncle Sam is backing you up, banks are willing to take a bigger risk on you.

- Who is this for?

Buyers with lower credit scores (as low as 500-580) or higher debt loads. If you have a few “dings” on your credit report from college, this is your safety net. - The Specs:

- Down Payment: 3.5% (if your score is 580+).

- Credit Score: Can go as low as 500 (but you’ll need 10% down).

- The Pros:

- Easier Approval: You can have a higher Debt-to-Income ratio. I’ve seen clients get approved for an FHA loan with a DTI of 50% or more.

- Low Rates: Believe it or not, FHA interest rates are often lower than conventional rates because the government guarantee makes them safer for the bank.

- The Cons (The “PMI Trap”):

Here is the catch. With an FHA loan, you pay a Mortgage Insurance Premium (MIP).- Upfront Fee: 1.75% of the loan amount added to your balance.

- Monthly Fee: You pay this every month.

- The Kicker: If you put down less than 10%, this insurance never goes away. Even if you pay off 99% of the house, you still pay the insurance. The only way to get rid of it is to refinance into a Conventional loan later.

My Take: FHA is a fantastic tool to get your foot in the door. Don’t be afraid of it. Just plan to refinance out of it in 3-5 years once your credit improves and your home value goes up.

3. The VA Loan (The “Gold Standard”)

If you served in the military, are on active duty, or are a surviving spouse, stop reading and get this loan. It is, hands down, the best mortgage product on the planet.

- Who is this for?

Veterans and eligible service members. - The Specs:

- Down Payment: 0%. Zero. Zilch.

- PMI: None. Never.

- The Pros:

- Interest Rates: usually the lowest on the market.

- Forgiving Credit: I’ve seen VA loans get approved with scores in the low 600s with excellent terms.

- Closing Cost Limits: The VA limits what fees lenders can charge you.

- The Cons:

- Funding Fee: There is a one-time fee (usually 2.3% for first-time use) rolled into the loan. However, if you have a service-connected disability (even 10%), this fee is waived entirely.

- Property Condition: The appraiser will be picky. The house must be safe, sound, and sanitary. No fixer-uppers with peeling paint or broken windows.

My Take: If you are eligible, use it. It is the only way to buy a house with zero money down and zero mortgage insurance. It’s a benefit you earned—don’t let a lender talk you into anything else.

4. The USDA Loan (The “Country Living” Loan)

This is the most misunderstood loan in America. People hear “USDA” and think they need to buy a farm or live in the middle of a cornfield.

Not true.

The USDA (United States Department of Agriculture) loan is designed to develop rural areas, but its definition of “rural” is very loose. Many suburbs just 20 minutes outside of major cities qualify.

- Who is this for?

People willing to commute a little further who have low-to-moderate income. - The Specs:

- Down Payment: 0%.

- PMI: It has a guarantee fee, but it’s much cheaper than FHA mortgage insurance.

- The Catch:

- Location: The home must be in a designated USDA zone. (You can check any address on their website map.

- Income Limits: You cannot make too much money. If you are a high earner, you are disqualified. The limits vary by county and family size.

My Take: If you don’t mind living on the outskirts of town, check the map. Getting a 0% down loan without being a veteran is a massive advantage.

The “Renovation” Wildcards

What if the only house you can afford is ugly? Like, “shag carpet in the bathroom” ugly?

Most first-time buyers think they have to buy a “move-in ready” home. But you can actually borrow the money to buy the house and fix it up in one single loan.

- FHA 203(k) Loan: This bundles the purchase price + renovation costs. You can fix the roof, upgrade the kitchen, or add a bathroom.

- Fannie Mae HomeStyle: The conventional version of the renovation loan. Harder to qualify for, but allows for “luxury” upgrades like a pool (which FHA doesn’t).

Why consider this?

Competition. Everyone is fighting for the pretty house. Nobody is fighting for the house with the broken porch. If you are willing to deal with the dust, you can build instant equity.

The “Secret Sauce”: The Mortgage Credit Certificate (MCC)

Okay, I promised you something you won’t find in the generic “How to Buy a House” pamphlets.

Most people focus on the interest rate deduction. You’ve heard of it: come tax season, you deduct the interest you paid from your taxable income. It saves you a little bit.

But there is something better: The Mortgage Credit Certificate (MCC).

This is not a deduction. It is a Tax Credit.

- How it works: A deduction lowers the income you are taxed on. A credit is a dollar-for-dollar reduction of the taxes you owe.

- ** The Math:** If you get an MCC for 20% of your mortgage interest and you pay $10,000 in interest that year, you get a $2,000 direct tax credit.

- The kicker: Some lenders can structure this so it boosts your monthly income for qualification purposes, helping you buy a more expensive house.

How to get it:

It is a state-specific program. You have to ask for it before you close. Once you close, it’s gone forever.

Action Step: When you interview a loan officer, ask: “Are you approved to offer the MCC program in this state?” If they say “What’s that?”, hang up. Find a pro who knows.

The Action Plan: Your 5-Step Roadmap

Information without action is just trivia. Here is exactly what you need to do, in order, to pick the right loan.

Step 1: Pull Your Real Scores

Don’t rely on Credit Karma. It uses a scoring model (VantageScore) that mortgage lenders do not use.

Go to AnnualCreditReport.com (it’s free) or pay for a FICO score report. You need to know your FICO 2, 4, and 5 scores.

- 620+: Aim for Conventional.

- 580-619: Look at FHA.

- Veteran? Go VA regardless of score.

Step 2: The “Assets” Check

Open your banking app. How much liquid cash do you actually have?

- Remember, you need cash for the Down Payment (3% – 3.5%) PLUS Closing Costs (usually another 2% – 4% of the price).

- If you have $0 saved: Look at USDA, VA, or ask your lender about Down Payment Assistance (DPA) grants in your state.

Step 3: Interview 3 Lenders (The “Rule of Three”)

Never, ever go with the first person you talk to.

Call:

- Your local bank/credit union.

- An online lender (like Rocket or Better).

- A local mortgage broker. (Do not skip this one. Brokers have access to wholesale rates that banks don’t have

Step 4: Ask the “Breakeven” Question

When comparing a Conventional loan (higher rate, no permanent PMI) vs. an FHA (lower rate, permanent PMI), ask the loan officer to run a “Total Cost Analysis” for 5 years.

Ask: “If I keep this loan for 7 years, which one actually costs me less total cash?”

The answer often surprises people.

Step 5: Get a “Verified” Pre-Approval

A pre-qualification letter is written on a napkin. It means nothing.

Ask your lender for a Fully Underwritten Pre-Approval. This means an actual human underwriter has reviewed your W2s and bank statements.

In a hot market, this is as good as cash. It tells the seller you are a sure thing.

A Final Reality Check (From a Friend)

Buying a house is stressful. There will be a moment during this process where you feel like you are bleeding money. You will pay for an inspection, an appraisal, and credit reports, and you might feel like you’re just handing out cash.

That is normal.

But choosing the right loan type is the foundation of your financial future.

- If you choose Conventional, you are betting on your strong credit to save you money long-term.

- If you choose FHA, you are using leverage to get into a home sooner rather than later.

- If you choose VA or USDA, you are smart enough to use the zero-down benefits available to you.

Don’t let the fear of “debt” keep you renting forever. Rent is an interest rate of 100%.

Your Homework:

Stop Zillow surfing for five minutes.

Call a local mortgage broker today. Not a bank teller—a broker. Tell them: “I am a first-time buyer. I want to compare a Conventional 97 vs. an FHA loan, and I want to check my eligibility for MCC tax credits.”

Watch their jaw drop because you know what you’re talking about. Then, go get those keys.

You’ve got this.

Frequently Asked Questions

1. Can I switch loan types later?

Yes! This is called refinancing. Many people start with an FHA loan to get into the house, improve their credit for two years, and then refinance into a Conventional loan to eliminate the mortgage insurance. You aren’t married to your loan forever.

2. Are “First-Time Buyer Programs” a specific type of loan?

Usually, no. When people say this, they are often referring to Down Payment Assistance (DPA) programs. These are grants or second loans that sit on top of your main mortgage (FHA or Conventional) to help cover your cash to close.

3. Why would anyone choose FHA if Conventional allows 3% down?

It comes down to the interest rate and debt ratios. If you have a 640 credit score, a Conventional loan might charge you a 7.5% interest rate + expensive PMI. That same person might get a 6.5% rate on FHA. Even with the permanent insurance, the monthly payment might be cheaper on FHA.

4. What is the biggest mistake first-time buyers make with loans?

They buy the maximum amount the bank approves them for. Just because the bank says you can borrow $400,000 doesn’t mean you should. Stick to a monthly payment you are comfortable with, not the max number on the pre-approval letter.